Top News

New #mathz: Bidenomics not adding up to happy, happy, joy, joy

I started looking around a little harder yesterday after doing my post on Fourth of July cook-out costs in the era of Bidenomics. The conflicting numbers and media massaging of the same for the rosiest take on bad news had me wondering if there were some hard calculations already being toted up in less friendly quarters.

There are, by George.

The first thing that shot the markets today was a jobs number that was way out of whack with both expectations and evidence on the ground from employers and those who track such things.

Private sector jobs increased by 497,000 in June, according to data from payroll processing firm ADP, in the biggest monthly gain since July 2022. June’s increase was more than double the Dow Jones consensus estimate of 220,000 and far better than the downwardly revised 267,000-job addition seen in May. The 2-year U.S. Treasury yield hit a 16-year high in Thursday’s session.

The ADP data, which is often unreliable and considered more volatile than other employment data, comes ahead of Friday’s official June payrolls report. Economists are expecting 240,000 non-farm payrolls were added last month, a slowing from the 339,000 jobs added in May, according to Dow Jones.

The ADP report was enough to spook the stock market into a 366+ point slide on fears that Jerome Powell will continue aggressively raising interest rates. What do jobs have to do with what the Fed does for monetary policy? Normally they wouldn’t factor as largely, but with Powell? He is myopic about the jobs numbers.

CNBC said mortgage rates “soared” on the data. That’s grim.

For a homebuyer taking out a $400,000 mortgage, the monthly payment of principal and interest rose to $2,720 from $2,637 in just a week.

The average rate on the popular 30-year fixed mortgage hit 7.22% on Thursday, according to Mortgage News Daily. That’s the highest point since early November.

Mortgage rates follow loosely the yield on the 10-year Treasury, which leapt higher following a much stronger-than-expected employment report from ADP.

What those interest rates have done so far to the mortgage business was pretty graphically illustrated in another chart another financial type had up yesterday. Take a gander at what the median house price is in your neck of the woods – ours in Pensacola was $350K in May – and then feast your eyes on these numbers.

With the increase in mortgage rates from 3% to over 7%, a $400k house will now cost you over $1,000,000.

🔥🔥🔥 pic.twitter.com/c0rQJBLUls

— Wall Street Silver (@WallStreetSilv) July 6, 2023

Any metro area is going to implode under the weight of this, and the worst part is that 7% may shortly look like a steal.

Now there was a time back in the 80s when the Fed’s prime rate hit an astronomical 20%, and I know everybody can remember their folks being thrilled with a 12 or 14% mortgage, but that was on a $60K bungalow in the burbs.

When your average crib is running $350K and apartment rents are thousands of dollars? Nobody can save up and nobody can move out. And the pool to buy your house for what you’d like to sell it for if you have to move is rapidly shrinking.

Nobody’s going to be buying anything.

In Canada it’s already so bad, they’re running fixed payment, variable mortgages out to 90 years! Almost sound like a student loan, doesn’t it?

…For most homeowners, the standard time to pay off a mortgage is 25 years.

Now, in the face of crippling interest rates, some existing homeowners are seeing their amortization period go as high as 90-years as their ‘fixed-payment’ variable-rate mortgages adjust automatically to rising interest rates.

“We’ve seen 60 years, 70 years, and we did see someone with 90 years,” said mortgage broke Ron Butler. “The majority of mortgages at some of the major banks are being extended and homeowners are getting concerned.”

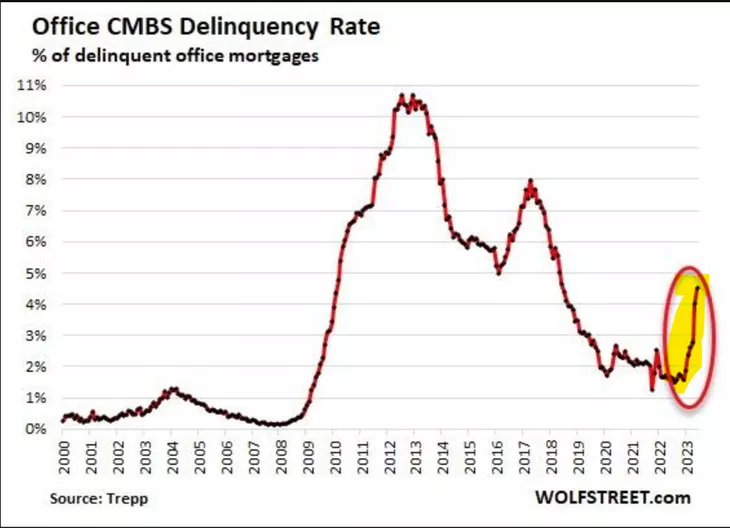

On the commercial real estate side, where variable rates and mortgage backed securities are the way they do business, June was an especially alarming month – the commercial mortgage backed securities (CMBS) delinquency index suffered the largest six-month spike since 2000. As we’ve pointed out with San Francisco’s vast amount of open office space, it’s only going to get worse.

…The mortgages – as we have seen in the current wave of defaults, including those where the landlord has just walked away from the property – are often variable-rate. Landlords liked variable-rate mortgages because they offer a lower interest rate, compared to fixed rate mortgages. And investors liked them because when rates go up, investors get a higher return, and the market value of the mortgage is largely protected.

But when rates go up a lot, as they have done since March 2022, the interest payments go up a lot, and by late last year, these interest payments began to double, and suddenly the building doesn’t pencil out anymore because rents, especially at office towers that are partially vacant, won’t cover the interest payments.

Those offices will most probably never be filled again, even if someone could wave a magic wand and straighten out the rate hikes.

…So this is going to be interesting because we’re just at the beginning of a massive structural change – not a temporary blip – that is impacting office towers; turns out, companies have figured out they won’t ever need this vast amount of vacant office space.

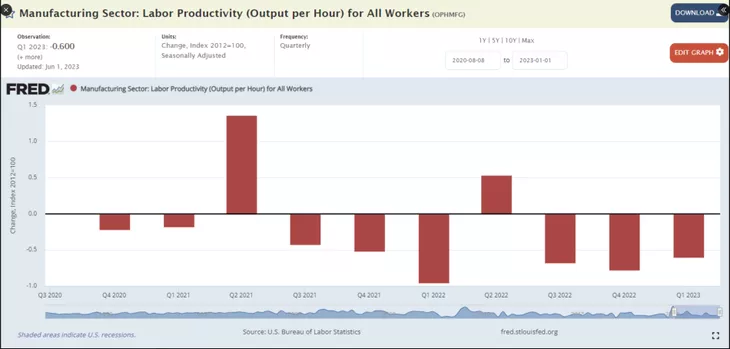

And what about that job that can pay for a home mortgage? Manufacturing has been on the slide for 8 months, contrary to everything the French Lady insists.

She does it too. They tell you what they spent, no word on results…

Manufacturing has been in decline for the last 8 months and the rate of decline is accelerating.#bidenomics. https://t.co/pOYDUKTNNB pic.twitter.com/8dRMzzPSKF— Frog Capital (@FrogNews) July 6, 2023

This is the St. Louis Federal Reserve’s own chart.

Yup. Biden has his best people on spreading the Bidenomics gospel.

HIS BEST

.@SecretaryPete here to take over the White House account as we hit the road talking Bidenomics and announcing the Biden-Harris Administration’s investments in our nation’s infrastructure. pic.twitter.com/Wqbv7xD9dY

— The White House (@WhiteHouse) July 6, 2023

Is it any wonder the WEF and globalists are in such a dang rush to move the peasants away from cash, checks, etc., and into something the elites can control for what expenditures they will allow them?

This guy at the WEF gets excited talking about the possibilities of a CBDC that can limit people from buying guns and ammunition ⚠️

— Wall Street Silver (@WallStreetSilv) July 6, 2023

“I’m terribly sorry, sir. Pitchforks aren’t on the approved list, and you weren’t authorized to be in the hardware store today. You are a designated data clerk. Security has been alerted.”

Bidenomics. Doesn’t add up to anything good.

Read the full article here

‘Googlers against genocide’ lead sit-ins, protests coast-to-coast at tech giant’s offices

Will Trump’s Criminal Trials Matter in November?

Stephen A. Smith: ‘Get Trump’ Lawfare Is Proof Democrats ‘Scared’ & ‘Can’t Beat Him On The Issues’

REALLY? Singer John Legend Claims Trump is ‘Benefiting’ From Two-Tiered Justice System (VIDEO)

Two Juveniles Accused of Vandalizing Catholic Church in Kentucky

Greg Kelly: Joe Biden isn’t a man of ‘excellence’ or ‘skill’

Ted Nugent: ATF ‘has lost its soul’

Carl Higbie: There is ‘no open mind’ at NPR anymore

I would support FISA reform, constraints on FBI: Harriet Hageman | The Chris Salcedo Show